The World Bank forecasts Myanmar’s GDP to grow by 3% in the year ending September 2023, with the recovery from the shocks of COVID-19 and the military takeover expected to remain subdued in the near term.

Under the current forecast, published in the World Bank’s January Economic Monitor report, the economy in September 2023 would still be around 13% smaller than in 2019, contrasting with the recoveries seen in other parts of the region.

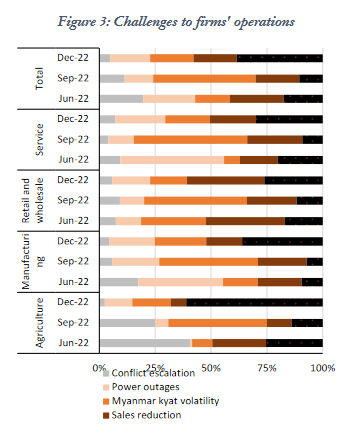

Business operations continue to be hampered by ongoing conflict, electricity shortages, and changing rules and regulations, while consumer demand remains weak amid stretched household incomes.

Inflation rose significantly in 2022, driven by rising fuel price increases and kyat depreciation, peaking at 19.5% in July 2022.

Nevertheless, the World Bank’s latest round of business surveys in December 2022 found that firms had generally recovered from the disruptions of forex exchange restrictions and kyat volatility, which had previously been the most commonly cited challenges.

Firms reported operating at 67% of capacity, in line with March and an improvement from June to September, and the share of firms not reporting any challenges to operations increased to 38%.

However, there is significant variation across sectors with manufacturers and retail and wholesale firms still operating below March levels and expected to face weakening export and domestic demand and agricultural and other service-oriented firms tipped to continue to improve as inflationary pressures ease.

The World Bank notes that there are some slight indicators of an improvement in domestic investment, prompted in part by the military administration’s import substitution policy with goods such as processed food now being produced locally.

However, foreign investment remains weak, with approved commitments totalling around $1.46bn in H2 2022, according to DICA data.

Of this, 83% was approved in July alone, coming from six Singaporean solar power firms, Singapore’s SIM Co Ltd to develop ports and stores to provide services for the offshore drilling industry, and Chinese garment manufacturer Best Garment Myanmar.

Electricity supply

The most recent edition of the Economic Monitor cites widespread outages as an ongoing challenge that has impacted households and businesses, including constraining manufacturing operations. Some businesses are able to afford diesel generators to continue operations while power is scarce, though higher fuel prices represent an additional expense. Businesses have also sought to procure solar backup power sources.

Power outages were temporarily reduced following the onset of the rainy season in 2022 but resumed around October as the electricity ministry sought to conserve hydropower generation capacity. While local authorities have announced power cuts on a rotating 3 to 5 hour basis in Yangon, in reality, outages are more frequent and erratic. The situation is worse in other parts of the country, and it is expected that during the dry season between January and April 2023, outages will worsen, particularly in areas with ongoing conflict.

The World Bank cites data indicating that daily peak generation declined from 3,878MW in November 2020 to 2,635MW in December 2022, due to a reduction in supply and the deterioration of infrastructure. Electricity losses on monthly generation are currently estimated at around 20%, compared to a global average of 8%.

Causes for the worsening outages and reduced power supply are identified as follows:

- The suspension of operations of gas-fired power plants, including CNTIC-VPower’s LNG-to-power projects, as well as delays in the completion of new projects and a slowdown in investment in the power sector following the military takeover.

- A lack of maintenance of existing electricity infrastructure due to labor strikes and a reduction in operating budgets resulting from lower electricity bill payment rates.

- Poor maintenance of natural gas pipelines connecting the Yadana and Zawtika offshore areas to power plants in Yangon, resulting in reduced capacity.

- Attacks on strategic power infrastructure and electricity offices, posing challenges to their security.

Natural gas production and exports

Despite changes in the ownership of several offshore producing areas in 2022, oil and natural gas production remained resilient.

Data from the Thai energy ministry indicates that export volumes received from the Yadana offshore area increased 5% between October 2021 and September 2022, while exports from Yetagun were up 57% year-on-year. These increases have offset a slight decline in exports from the Zawtika offshore area.

Though production at Yetagun has increased following the appointment of Northern Gulf Petroleum, output is still low in absolute terms and expected to remain so over the medium term, as the field is nearly depleted. Meanwhile, PTTEP has continued to make progress on the development plan of Zawtika, issuing contracts for four new wellhead platforms to be constructed under Phase 1D of the project.

Data also indicates an increase in the value of Myanmar’s gas exports to China from June 2022, likely a result of higher global prices for oil and gas, though export volumes have remained fairly constant.

Fuel prices remain high despite declines in global prices

As mentioned above, the sharp rise in inflation throughout FY2022 can be largely attributed to the combined effect of rising fuel prices and the depreciation of the kyat. Fuel price increases throughout 2022 were initially driven by higher global prices, at least in part. However, from May onward, global prices began to decline, while domestic fuel prices remained high.

These persistent high prices can mainly be attributed to the exchange rate depreciation as well as fuel scarcity caused by a combination of foreign exchange restrictions, new state intervention in the fuel sector and factors such as conflict in some areas. Fuel stations in many areas of the country, including the urban centers of Yangon and Mandalay, have had to ration fuel and shut down operations (sometimes permanently), especially when the regulated reference prices have been lower than the cost price of fuel.

State finances and energy SOE revenues

The report notes that the fiscal position has strengthened, with aggregate revenue collection improving in the six months to March 2022, due to increased income of state-owned enterprises (SOEs) and and improved tax collection. Revenues were around 3 percentage points of GDP higher than the previous year.

Ministry of Planning and Finance and World Bank estimates show that tax revenue has rebounded to 5.3% of GDP in annualised terms in the six months to March 2022. Recent World Bank firm surveys show that the share of firms paying taxes to the authorities increased between December 2021 and June 2022 and was close to 2020 levels, but then declined in the September quarter.

Meanwhile, non-tax revenue from SOEs was boosted by higher-than-projected profits in energy in the six months to March 2022. Energy enterprises recorded a profit equivalent to around 0.4% of GDP against the original estimate of a loss of 0.1% of GDP.

Overall, the energy SOEs’ revenue amounted to around 4.3 percent of GDP, equivalent to around 38% of overall revenue in the six months to March 2022, the report said, most of which comes from Myanma Oil and Gas Enterprise (MOGE), whose revenue is estimated to contribute about 70% of all energy SOE revenue.